The finding here is one we should have been able to get to through logic. So, when an interest rate change is announced, if interest rates were around normal levels then this boosts bank equity prices. Because lowering those rates – and what is being measured is whether rates were lowered by more than expected – boosts the economy and a boosted economy is good for bank profits. More people will borrow, more borrowers will be able to repay etc. But when interest rates are already on the floor the same lowering by more than expected reduces bank equity prices. The reason being that banks live off interest rate differentials. The effect is larger on banks which largely fund from customer deposits. Which makes sense, as zero is that lower bound there. Falling lending rates thus compresses the interest differential:

Monetary policy and bank equity values in a time of low and negative interest rates

Miguel Ampudia, Skander Van den Heuvel 17 July 2019

The effects of interest rate surprises on banks are different when nominal interest rates are very low. This column reveals how, in ‘normal’ times, policy rate announcements that are below market expectations tend to boost banks’ stock prices on average. When interest rates are very low, however, there is a reversal of this effect, with negative rate surprises reducing banks’ stock prices. This negative impact is larger for banks whose funding relies more on retail deposits than on other sources of funding.

In July 2012, the ECB lowered its deposit facility rate – the interest rate that banks receive for depositing money with the central bank overnight – to 0%. A series of further cuts pushed the deposit facility rate into negative territory, reaching -0.4% in March 2016. These cuts were intended to provide more monetary accommodation amid low inflation and weak economic conditions. But they also led to a debate regarding the effects of very low interest rates on the economy. Low rates can strengthen economic conditions by boosting aggregate demand, but they also raise concerns because, by reducing the income from interest-bearing assets, they may hurt the profitability of banks. Monitoring the effects of interest rate policy on the behaviour of banks is important for policymakers, because of the central role played by banks in the transmission of monetary policy and the importance of credit for economic activity.

Recent evidence on the effect of very low interest rates on banks is mixed. Heider et al. (2019), for instance, have found that negative interest rates reduce the net worth of some banks. Other studies, however, have found that they have a positive effect on bank profits and lending (e.g. Altavilla et al. 2018, 2019). In this column, we complement existing evidence by focusing on the effect of very low interest rate on banks’ stock prices. Because stock prices reflect expectations about future profitability, their evolution provides forward-looking information that may not be fully captured by banks’ current profits or their lending behaviour.

Identification of monetary policy shocks

In order to answer our question, we must overcome two methodological challenges. The first is to isolate the effects of changes in interest rates – if interest rates are often lowered when the economy is weak, and banks’ stock values also tend to decline when the economy is weak, then low interest rates and low stock values are bound to be observed together even if low rates do not lead to lower bank stock prices. So how can we distinguish between changes in banks’ equity values that are driven by the interest from those driven by underlying economic conditions? The second challenge is that, if changes in interest rates are anticipated by financial markets, they will react in advance and it may be hard to observe any reaction at the time of a policy rate announcement. In order to solve these challenges, we use high-frequency data in an event study approach, adapting the methodology first developed by Kuttner (2001) to the euro area setting. We use this methodology to identify interest rate surprises around monetary policy announcements.

Here is how it works. For each press statement released after an ECB Governing Council meeting,1 we construct a short-term interest rate surprise. The surprise is calculated as the change in the price of the euro overnight index average (EONIA) swap contract with a maturity of one month in a narrow window around the press statement (the ‘event’). For each statement, we construct an ‘event window’ that extends from 10 minutes before the release until 20 minutes after it. The change in the EONIA swap rate between the start and end of the window represents the unexpected change in the level of the ECB’s policy interest rate, i.e. the monetary policy shock. As an intuitive example, picture a case in which the market is fully anticipating a rate cut, perhaps because the economy appears to be weakening. Then, the expected rate is already reflected in the price of the swap, which will therefore be unaffected by if the ECB effectively decides to cut the policy rate according to expectations. In this case, the interest rate surprise is equal to zero. If the ECB decides instead to cut rates more than expected (less than expected), we say that the interest rate surprise is negative (positive).

We repeat the same procedure using the two-year EONIA swap contract.2 Thus, we construct both a short-term rate surprise and a long-term rate surprise.3

The impact of monetary policy surprises over time

After constructing our interest rate surprise, we assess how it affects the stock price of European banks. In particular, we analyse the ability of surprises to explain changes in the stock price of banks in a 30-minute window around the release of the press statement. We do so by conducting a regression analysis using our interest rate surprises.4 We divide our sample into three periods. The first is the pre-crisis period, from the beginning of our sample period until the failure of Lehman Brothers. The second is the crisis period, from the failure of Lehman Brothers until the setting of the ECB’s deposit facility rate to zero. The third is the period of very low and negative interest rates, from the setting of the ECB’s deposit facility rate to zero until the end of the sample period.

In the first two periods, negative rate surprises had a positive effect on banks’ equity values, an effect that became stronger after the crisis started. In the pre-crisis period, a 25-basis point negative surprise resulted in an average increase of 0.76% in bank stock prices, while in the crisis period a negative surprise of the same magnitude boosted bank equity values on average by 1.3%. However, these effects reversed during the period of very low and negative rates. In this environment, negative rate surprises were detrimental to bank equity values. We find that a 25-basis point negative surprise lowered bank equity values by 2.0% during this period.

The impact of monetary policy surprises across banks

What explains our results? What is the mechanism underpinning our findings? One general channel, which we do not consider here, is that monetary policy provides information about the economic outlook: a negative interest rate surprise, for instance, may signal that the economic outlook is weaker than expected thereby leading to a decline in stock prices.5 But interest rate surprises also affect banks through more direct channels, such as (i) changes in net interest margins; (ii) the revaluation of long-term assets on the balance sheet; and (iii) changes in the demand for loans and deposits, asset quality, and off-balance sheet positions. While many of these direct channels have similar effects on banks’ profits whether rates are high or low, some do not.

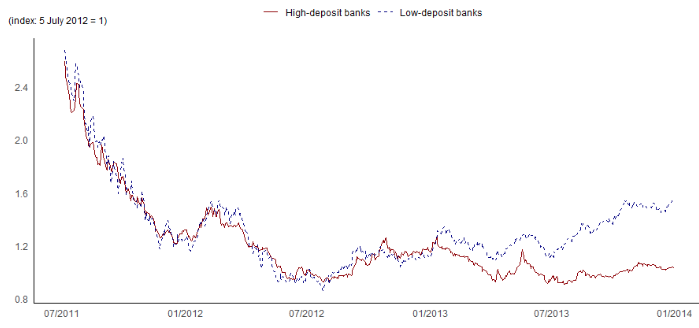

In particular, the effect of interest rate surprises on net interest margins is likely to change in a very low interest rate environment. The reason is that banks are reluctant to pay negative rates on deposits to retail customers.6 This means that, when short-term rates are already close to zero, further declines in short-term rates are likely to squeeze the net interest margins of deposit-intensive banks, as their borrowing costs do not fall as much as market rates, potentially hurting their profitability. Banks that rely more on other types of funding (e.g. wholesale funding), in contrast, should not be hurt as much by negative rates, since they can pass on these negative rates in their funding. Figure 1 provides preliminary evidence corroborating this hypothesis: deposit-intensive banks underperformed relative to low-deposit banks over the period in which short-term rates dropped to zero and below.

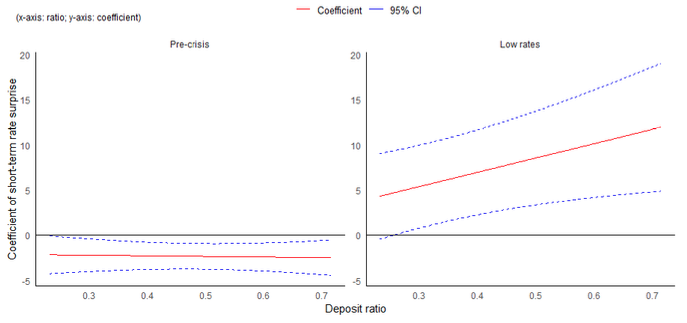

To further investigate whether the deposit channel is behind our results, we test this prediction, again with a regression analysis. In the analysis, we interact our rate surprises with the level of the deposit ratios of the banks in our sample (and also our sample sub-periods). The coefficients of these interaction terms indicate how the relationship observed between interest rate surprises and stock returns depends on banks’ funding models: a positive coefficient indicates that the effect of negative rate surprises on banks’ stock prices is stronger for banks with high deposit ratios. Results from this regression analysis are summarised in Figure 2.

In normal times, illustrated in the left panel of the chart, negative rate surprises appear to benefit all banks in a similar way, irrespective of their funding structure. A 100-basis point negative interest rate surprise raises the stock prices of banks by about 2 to 2.5%. In the period of very low and negative rates the effects are reversed, as we have already seen. Moreover, as the right panel shows, the differential effects across bank types are substantially more pronounced than in normal times. Specifically, during the very low and negative rate period, deposit-intensive banks exhibit much larger declines in their equity values in response to negative rate surprises than banks that rely less on deposit funding. The decline for a ‘high-deposit bank’ is almost 8 percentage points higher than for a ‘low-deposit bank’.

Figure 1 Evolution of stock prices of high and low-deposit banks

Notes: The figure shows the average stock price, normalised to 1 on 5 July 2012 for each stock, for banks in the highest and lowest quartiles of the deposit ratio distribution.

Figure 2 Response of banks’ stock values to rate surprises: The role of deposits

Notes: The figure shows the estimated impact and 95% confidence intervals (CI) of the short-term rate surprise on bank equity values as a function of banks’ deposit ratios. For ease of presentation, the sample mean of the trend in the deposit ratio is added back to its de-trended ratio. The left panel shows the pre-crisis period and the right panel shows the very low/negative rate period.

Concluding remarks

During normal times, negative interest rate surprises have a positive effect on the stock prices of banks. The research presented here shows that things are different when interest rates are very low or negative. In such an environment, negative interest rate surprises seem to have a negative effect on banks’ stock prices. This reversal, moreover, is much larger for banks that rely more on deposit funding.

Let us conclude where we started: low interest rates have many effects of the economy, not all of which operate through banks. And even those effects that do operate through banks are multi-layered, with some studies showing that negative rates can reduce the net worth of some banks (e.g. Heider et al. 2019) while others showing that negative rates may actually boost profits and lending by some banks (e.g. Altavilla et al. 2018, 2019). Our study complements existing evidence by documenting the effect of interest rate surprises on banks’ stock prices in low-interest rate environments. Ultimately, a holistic view of low interest rates must consider all of these effects jointly. This is an exciting research agenda going forward.

{kind=link}