This is useful evidence that markets are working as markets should do. There is a risk that some fossil fuel reserves will not be usable as a result of policy changes concerning climate change. It’s a much smaller issue that the alarmists assume simply because fossil fuel firms are not valued upon reserves which might be exploited out a decade or three. Standard market discounting to net present value of future revenues takes care of that.

However, we can look for more subtle signs that the financial system is accounting for the risk.When we look we find exactly that. There is no carbon bubble therefore, stranded carbon assets are not a risk to systemic resilience:

The 2015 Paris Climate Agreement to limit the rise in global warming to 2°C compared to pre-industrial levels requires massive reductions in CO2 emissions in the next decades and near zero overall greenhouse gas (GHG) emissions from the next century onward. The limiting of total carbon emissions will leave the majority of fossil fuel reservesas ‘stranded assets’ (Carbon Tracker Initiative 2011, 2013, McGlade and Ekins 2015), with companies owing fossil fuel unable to use most of their reserves. The large fraction of potentially unburnable fossil fuels poses substantial financial risk to fossil fuel companies. Nevertheless, fossil fuel firms still largely invest in locating and developing new fossil fuel reserves (Carbon Tracker Initiative 2013). This ongoing investment, together with the already large fraction of potentially stranded assets, suggests that financial markets neglect the possibility that fossil fuel reserves become ‘stranded’ resulting in a ‘carbon bubble’, i.e. that fossil fuel firms are overvalued.

The potential effects of a carbon bubble on financial stability have been recently discussed in the academic literature (Weyzig et al. 2014, Schoenmaker et al. 2015, Batten et al. 2016) and are increasingly appearing on the agenda of regulators and supervisors (Bank of England 2015, Carney 2015, ESRB 2016). However, there is no clear evidence if whether, and to what extent, investors price the risk of unburnable carbon. Studying equity markets, recent research identifies an insignificant impact of climate/technology news on fossil fuel firms’ abnormal returns (Batten et al. 2016, Byrd and Cooperman 2016). This insignificant impact could be due to investors’ difficulties in assessing credible future climate policies and their impact on carbon-intense sectors, to investors believing in climate policy inaction, or to already accurately priced risk of climate-related stranded fossil fuels (Batten et al. 2016, Byrd and Cooperman 2016). Thus, we are missing insights into the effect of climate policy risk on the pricing of financial products.

Is there a carbon bubble in the corporate loan market?

In a recent paper, we provide the first evidence for climate policy risk pricing, using evidence from the corporate loan market (Delis et al. 2018). Carbon-intensive sectors are largely debt financed, implying that the impact of stranded fossil fuels can easily spill over to the banking sector. This almost naturally generates the question of whether banks consider the risk that fossil fuel reserves will become stranded when originating or extending credit to fossil fuel firms. Essentially, this implies that if banks thoroughly consider the risk of climate policy exposure in the pricing of corporate loans, then no carbon bubble exists in the credit market.

Ideally, our main explanatory variable illustrating climate policy exposure would be the amount of stranded assets of a fossil fuel firm. However, such detailed estimates are not available. In principle, a devaluation of fossil fuel reserves can be caused by changes in regulation (policies), technologies, or carbon prices. Climate policies involve direct environmental regulations (e.g. pollution outputs and inputs) as well as stimulating the development of alternative technologies (for example, by subsidising instruments. The probability of stranded fossil fuel reserves is thus higher in countries with higher climate policy stringency. Therefore, we proxy the risk of stranded fossil fuel reserves by the risk of climate policy stringency, i.e. whether a country places considerable effort in climate change policies. A fossil fuel firm owing exploration rights for reserves in a country with strict climate policy faces a higher probability of reserves being stranded than a firm with fossil fuel reserves in a country with loose climate policy.

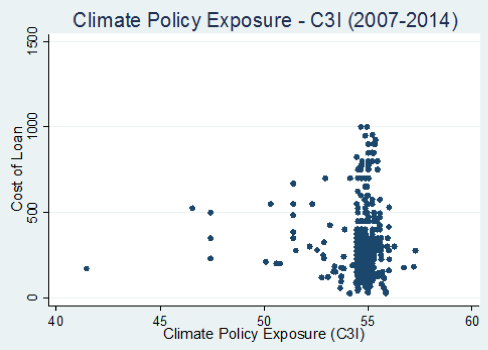

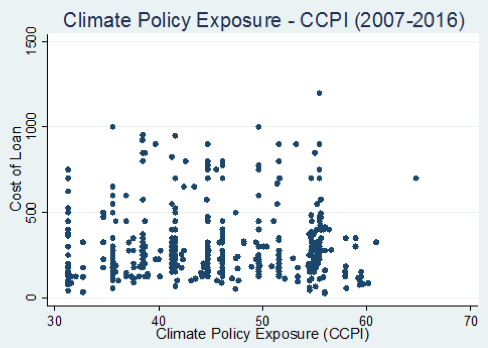

This implies that we require information on the total amount of fossil fuel reserves of firms across countries. As these data are not readily available in conventional databases, we hand-collect them from firms’ annual reports. Some firms hold fossil fuel reserves in more than one country, so we construct a relative measure of reserves for each firm, in each country, and in each year. Finally, we generate a firm-year measure of climate policy exposure (risk) from the product of relative reserves and either one of the Climate Change Cooperation Index (C3I) by Bernauer and Böhmelt (2013) or the Climate Change Policy Index (CCPI) by Germanwatch. These country-year indices, respectively available for the periods 1996-2014 and 2007-2017, reflect environmental policy stringency and thus risk.

Figure 1 Climate policy exposure and the cost of loan

Note: The cost of loan in basis points is defined as the loan spread plus any facility fee.

Our baseline analysis compares the loan pricing of fossil fuel firms to non-fossil fuel firms and the loan pricing among fossil fuel firms based on their climate policy exposure. We strengthen the validity of this model via the fielding of many control variables and fixed effects (e.g. loan type and purpose, bank*year, and firms’ country fixed effects). As relevant environmental policy initiatives are recent, our analysis covers the period 2007-2016. We identify further differences in loan pricing by comparing, in the pre- and post-2015 periods, the terms of lending of fossil fuel to non-fossil fuel firms based on their climate policy exposure. The year 2015 signals a turning point because of the Paris Agreement and the intensified discussion of a carbon bubble.

Our results: No evidence of pricing of climate policy risk prior to 2015, some pricing of risk after 2015

Our results from the full 2007-2016 sample are consistent with a carbon bubble in the corporate loan market.

- We find no evidence that banks charge significantly higher loan spreads to fossil fuel firms.

- We find some evidence for higher loan fees to fossil fuel firms, but even these results are economically small and not robust across different specifications.

- However, when looking into the post-2015 period, we find the first evidence that banks increased their loan spreads to fossil fuel firms that are significantly exposed to climate policy risk. The economic significance is rather small: a one standard deviation increase in our measure of climate policy exposure implies that risky fossil fuel firms from 2015 onward are, on average, given a 2-basis points higher AISD compared to less-exposed fossil fuel firms, non-fossil fuel firms, and themselves before 2015.

To give an impression of the magnitude of this effect, the 2-basis point increase implies an increase in the total cost of the loan with a mean amount ($19 million) and maturity (four years) of around $200,000. Then, we hand collect data on the dollar value of fossil fuel reserves and find that the mean fossil fuel firm in our sample holds approximately $4,679 million in such reserves. Thus, it seems unlikely that the corresponding increase that we identify in the post-2015 period covers the potential losses from stranded assets.

We further investigate this finding by using the actual value of the holdings of proved fossil fuel reserves, instead of simply examining average differences between the fossil fuel and non-fossil fuel firms. Retaining the dichotomy between the pre-2015 and post-2015 periods, we find that a one standard deviation increase in our measure of climate policy exposure implies an AISD that is higher by approximately 16 basis points for the fossil firm with mean proved reserves scaled by total firm assets in the post-2015 period versus the non-fossil fuel firm. This implies an increase in the total cost of borrowing for the mean loan of $1.5 million. This extra cost of borrowing represents noticeable evidence that banks are aware of the climate policy issue and started pricing the relevant risk post-2015.

We also document a direct negative effect of climate policy exposure on the maturity of loans to fossil fuel firms in the post-2015 period.Moreover, we show a tendency of fossil fuel firms to obtain slightly larger loans compared to non-fossil fuel firms when environmental policy becomes more stringent. Even though the respective increase in loan amounts is economically rather small, our finding is in line with a substitution effect due to higher environmental policy risk from ‘lost’ access to equity finance toward bank credit. Finally, we document a slightly higher loan pricing to fossil fuel firms by ‘green banks’ (i.e. those participating in the United Nations Environment Programme Finance Initiative) when climate policy risk increases.

{kind=link}

A market dependent entirely on inconstant subsidy, tax, planning decisions and fashion, not to mention as ever bad laws with unintended consequences? Well, you have to try to anticipate risk, but it’s just a guess, isn’t it?

Pricing in risks is what banks do, including the risk that the government will declare war against it. I bet loans to Microsoft had a premium while the Clinton Administration was trying to split it apart. Banks must consider the possibility that Eric Schneiderman’s lawsuit will prevail and ExxonMobil will be found guilty of securities fraud for not hyping Global Warming in its materials to inspectors….Huh? He what? I wonder, then, if ExxonMobil’s effective borrowing rate just went down a smidgen. PS — The above description of the Paris Accord puts it on absurd display. Mankind unanimously (except for the… Read more »