Yes, obviously, we all fall back in amazement as we contemplate the idea that Gordon Brown understood any part of economics. And yet he did and it was a major reason why we’re not in the euro today. How interest rates affect an economy will depends upon the structure of that economy. One major pathway being through mortgages and household budgets. A country with largely floating rate mortgages will be more leveraged to interest rate changes than one with fixed rate. Obviously enough, if everyone’s on a floating rate then changing interest rates changes everyones’ bill. A fixed rate system only changes the bill for new market entrants. The economies will thus react differently to changed interest rates.

Brown point out that the UK economy would change very differently from the German with respect to interest rates for this reason. He even tried to encourage long term fixed rate mortgages in order to close that gap. This paper is looking at a finer level of detail of the idea but shows the same basic structure. How an economy reacts to interest rate changes depends, in part, upon the structure of the housing finance market.

State-dependent effects of monetary policy: The refinancing channel

Martin Eichenbaum, Sérgio Rebelo, Arlene Wong 02 December 2018

Mortgage rate systems vary in practice across countries, and understanding the impact of these differences is critical to the design of optimal monetary policy. This column focuses on the US, where most mortgages have a fixed interest rate and no prepayment penalties, and demonstrates that the efficacy of monetary policy is state dependent, varying in a systematic way with the pool of potential savings from refinancing. As refinancing costs decline, the effects of monetary policy become less state dependent.

Housing markets play a critical role in the monetary transmission mechanism. Persistent changes in monetary policy rates affect both variable and fixed mortgage rates. Changes in the latter affect aggregate demand by affecting the volume of new mortgages, and the number of existing mortgages that are refinanced.1

Mortgage rate systems vary in practice across countries. Understanding the impact of those differences is critical to the design of optimal monetary policy, especially in an era when FinTech is changing key aspects of the mortgage market.

In the US, most mortgages have a fixed interest rate and no prepayment penalties. The decision to refinance depends on the potential savings relative to the refinancing costs. In a recent paper, we study how the impact of monetary policy depends on the distribution of potential savings from refinancing the existing pool of mortgages (Eichenbaum et al. 2018).

Our key finding is that the efficacy of monetary policy is state dependent, varying in a systematic way with the pool of potential savings from refinancing. We develop a model that is consistent with this finding and use it to study new trade-offs in the design of monetary policy as well as to assess the impact of FinTech-driven lower re-financing costs on the monetary transmission mechanism.

Potential savings from refinancing depend on a variety of factors, including old and new mortgage interest rates, outstanding balances and the precise refinancing strategy that a household pursues. We consider various measures in our analysis, focusing primarily on the gains from refinancing 30-year conforming mortgages. Our benchmark measure of potential savings is the average value of the difference between the mortgage rate on an existing mortgage and the new mortgage rate that a household could refinance at, controlling for the household’s location and credit worthiness (FICO) score. We refer to this difference as the interest-rate gap.

Our empirical work is primarily based on Core Logic Loan-Level Market Analytics, a loan-level panel data set with observations beginning in 1993 and, in our case, ending in 2007. The latter choice is motivated by the widespread view that credit constraints were much more prevalent during the financial crisis period (e.g. Mian and Sufi 2014, Beraja et al. 2018) than in the preceding period.

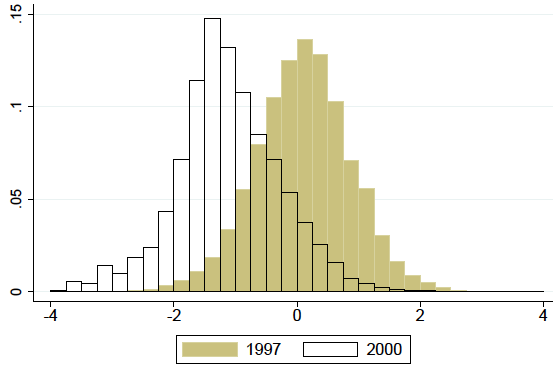

We find that the distribution of potential savings from refinancing varies a great deal over time[AW1] . Figure 1 displays the distribution of the interest-rate gap across mortgages in 1997Q4 and 2000Q4. The two distributions are very different. In 1997Q4, about 60% of mortgages had a positive interest-rate gap. In contrast, only 10% of mortgages had a positive interest-rate gap in 2000Q4. Similarly, the average interest-rate gap was much higher in 1997Q4 (0.55%) than in 2000Q4 (1.3%).

Figure 1 Interest rate gap (existing rate – new rate)

Notes: The figure depicts the distribution of interest-rate gaps across borrowers. The interest rate gap is defined as the difference between the existing mortgage rate and the current market rate. See Eichenbaum et al. (2018) for more details.

We implement an instrumental-variable strategy for measuring the effect of a change in the mortgage rate on the fraction of mortgages that are refinanced over the next year. Our instruments are based on high-frequency movements in the Federal Funds futures rate and the two-year Treasury bond yield in a small window of time around Federal Open Market Committee announcements

Our findings

Our empirical findings can be summarised as follows.

- First, we find a strong state-dependent effect of a change in mortgage rates on refinancing rates.

Consider for example the effect of a 25 basis point drop in mortgage rates. The marginal impact of a one standard deviation increase in the average interest-rate gap is 6.8%. Put differently, when the average interest gap is one standard deviation higher, a 25 basis point fall in the mortgage leads to 6.8% higher rise in the number of mortgages that are refinanced. This effect is large relative to the average annual refinancing rate of 8.5%.

- Second, we find that there are important state-dependent effects on the percentage of mortgages with cash-out refinancing (i.e. the balance of the new mortgages is higher than that of the old mortgages).

Cash-out refinancing is important because we know from Mian and Sufi (2014) that households predominantly use this type of refinancing to increase their consumption. This phenomenon plays a critical role in allowing our structural model to generate large effects from a fall in mortgage rates on aggregate consumption.

To assess the magnitude of state dependency in refinancing, consider the impact of a 25 basis point change in the mortgage rate on the fraction of total loans with cash-out refinancing over the next year. Our results imply that the marginal impact of a one standard deviation increase in the average interest-rate gap on cash-out refinancing is 6.2%. This effect is large relative to the average annual cash-out refinancing rate of 5.5%.

- Finally, we find that changes in monetary policy have important state-dependent effects on actual economic activity, as measured by the number of permits required for new privately owned residential buildings.2

A model to highlight new trade-offs in the design of monetary policy

Motivated by our empirical results, we construct a quantitative dynamic life-cycle model that highlights new trade-offs in the design of monetary policy. The key empirical properties of the model are as follows.

- First, it is consistent with the life-cycle dynamics of home-ownership rates, consumption of non-durable goods, household debt-to-income ratios, and net worth.

- Second, it accounts for the probability that a mortgage is refinanced conditional on the potential savings from doing so. It is also consistent with the fact that most households who refinance engage in cash-out refinancing.

- Third, and most importantly, the model accounts quantitatively for the state dependent nature of the effects of monetary policy on refinancing decisions that we document in our empirical work.

Our model implies that the effect of a given interest rate cut depends on the history of monetary policy choices. A given interest rate cut is less powerful when preceded by a sequence of rate hikes. When rates have been rising, many homeowners have existing fixed mortgage rates lower than the current market rate, and thus aren’t motivated to refinance in response to a modest fall in the interest rate. In contrast, a given interest rate cut is more powerful when preceded by a sequence of rate cuts. When rates have been falling, many homeowners have fixed mortgage rates that are higher than the current market rate, so are motivated to refinance in response to an interest rate cut.

We use our model to study how the efficacy of monetary policy and the state dependency of its effects are affected by a decline in refinancing costs. This question is particularly important because of the growing share of FinTech lenders in mortgage markets.

Our model implies that as refinancing costs decline, the effects of monetary policy become less state dependent. The intuition for this result is as follows. As refinancing costs decline, refinancing rates increase. This effect leads the distribution of savings from refinancing to vary less over time and to become more concentrated around zero. So, the effects of monetary policy become less state dependent.

The flip side of this result is that, as refinancing costs decline, monetary policy becomes more powerful. The intuition is as follows. In our model, many households face binding borrowing constraints. When refinancing costs decline, a given fall in interest rates induces more of these types of households to engage in cash-out refinancing. These households use the additional resources to boost consumption. More households respond in this way to a given fall in mortgage rate when refinancing costs decline.

Our analysis focuses on the effects of monetary policy in systems where mortgages have primarily fixed interest rates. However, there are many countries where mortgages have primarily variable interest rates, including Australia, Ireland, Korea, Spain, and the UK.

The state-dependent effects of monetary policy that arise through the refinancing channel in a fixed mortgage rate system do not arise in a variable mortgage rate system. The reason is that there are no unexploited refinancing opportunities in a variable mortgage rate system. So, even if FinTech succeeds in driving refinancing costs to very low levels, the housing channel of the monetary transmission mechanism in the US will not converge to that of countries with variable interest rate mortgages.

{kind=link}

No, Gordon didn’t want to join the Euro because he knew that if we did, his wizard wheeze of hiding public debt off-balance-sheet in order to buy baubles for his clients would be rumbled by the growth and stability pact. Oh, and Tony wanted to join the Euro.