It’s entirely true that the blockchain part of cryptocurrencies looks interesting. Might even have some useful real world applications other than reprising every monetary scam history has ever invented at warp speed. It doesn’t seem to be true though that such cryptocurrencies, Bitcoin and the like, have any particular use for central banks:

Central bank digital currency: Concepts and trends

Sayuri Shirai 06 March 2019

Recent years have seen the emergence of digital currencies such as Bitcoin as potential private sector money. Central banks are also considering whether to issue their own digital tokens to enable decentralised verification of transactions while maintaining attractive cash-like features. This column lays out the four existing proposals for implementing central bank digital currency. Due largely to technical constraints, however, central banks in general have not found a compelling reason to issue their own digital currency.

Money fulfils the basic functions of a medium of exchange, unit of account, store of value, and standard of deferred payment. To meet these four functions, it must be durable, portable, divisible, and difficult to counterfeit. While central banks and the private sector provide such money, digital tokens such as Bitcoin, using distributed ledger technology, have emerged over the past decade as potential money. Some central banks have experimented with the application of digital tokens in their businesses by issuing their own digital tokens – known as central bank digital currency (CBDC) – for various reasons. (Bech et al. 2018).

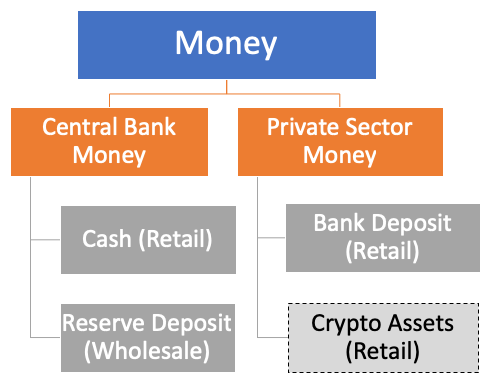

Central bank money and its features

A central bank has the sole right to issue paper notes (fiat money) to the general public and distribute them through commercial banks. While coins are issued mostly by the government as a supplement to central bank notes, in many cases they are also distributed by a central bank to the general public through commercial banks. Therefore, both notes and coins, or cash, can be viewed as central bank money (Figure 1). Central banks issue another type of money to commercial banks in the form of reserve balances at the central bank (reserve deposits). Sweden’s central bank, the Riksbank, has also been investigating the possibility of issuing deposit accounts to the general public.

Figure 1 Classification of money

Source: Prepared by the author.

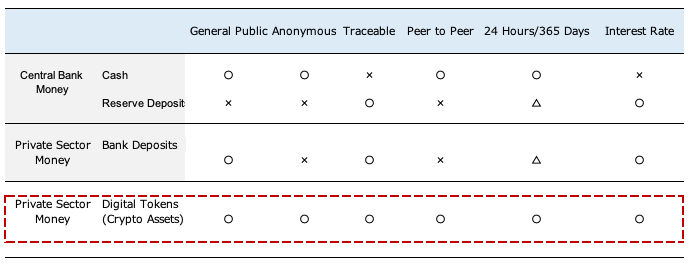

Cash and reserve deposits have different features (Table 1). Digital currency is available in digital form, in contrast to physical, visible cash. Cash is used mainly by the general public (and is thus called ‘retail central bank money’), is available 24 hours a day and 365 days a year, and is usable anywhere within an economy where the legal tender status prevails. In contrast, reserve deposits are available only to designated financial institutions such as commercial banks (and are thus called ‘wholesale central bank money’), and are used for managing the real-time interbank payments and settlements system. Wholesale central bank money is not necessarily available 24 hours a day or 365 days a year, although central banks have been making efforts to improve systems to enable faster and more efficient transactions.

Table 1 Main features of central bank money and private sector money

Source: Prepared by the author.

From the user’s perspective, the important difference between cash and reserve deposits is that cash is anonymous and cash transactions are non-traceable since transactions cannot be monitored by the central bank. In contrast, all the transactions based on reserve deposits are traceable by the time sequence of transactions made, since they are a digital representation of money that enables the recording of all footprints. Reserve deposits are non-anonymous since they are based on an account-based system that uses an owner register. In addition, cash provides a peer-to-peer settlement form, while reserve deposits are non-peer-to-peer settlements, as transactions between commercial banks are intermediated by a central bank. Because of this anonymity and non-traceability, cash is often preferred by the general public who wish to maintain privacy and is often used for money laundering and tax evasion purposes. Cash handling costs are high when considering not only the direct fees (i.e. the cost of paper and design fees to prevent counterfeiting) but also the security and personnel cost associated with the maintenance of cash provision and payment services by commercial banks, shops, firms, and individuals.

From the perspective of an issuer (a central bank), the important difference between cash and reserve deposits is the presence or absence of an interest rate. Cash is an interest rate-free instrument, while a positive or negative interest rate can be applied to reserve deposits. It is known that a negative interest rate policy can be a monetary policy tool below the effective lower bound. The policy can be more effective if commercial banks pass the increased costs on their retail bank deposits held by the general public to maintain interest margins and profits. This happens when the general public no longer utilises cash.

Private sector money and its features

The most important private sector money is bank deposits (Figure 1), which can be used to make payments using ATM cards, internet banking, and/or debit cards. Bank accounts can also be used to pay credit card companies by allowing them to debit payments for bills from accounts. Developments in digital wallets and cashless devices that facilitate payments through apps on smartphones by adding debit cards and credit cards have enabled faster and more efficient retail payments. While bank deposits are not legal tender, their values are denominated in legal tender and can be exchanged at a one-to-one value. Nonetheless, they are riskier than cash because the issuers could go bankrupt – although a deposit insurance system guarantees deposits of a failing bank up to a certain amount. Similar to reserve deposits, bank deposits are non-anonymous and transactions are traceable (Table 1). Bank deposits are a digital currency, so a positive or negative interest rate can be applied. Commercial banks generally refrain from charging a negative rate for fear of losing clients, and instead may quietly increase charges on their services (such as ATM usage fees). Real-time fast settlement systems are increasingly available 24 hours a day, 365 days a year for retail bank depositors in many countries. The size of bank deposits is much larger than the size of central bank money due to the large number of financial institutions and money creation activities, which generate deposits and loans.

In addition, new types of private sector money based on distributed ledger technology – often called digital tokens or crypto assets – have emerged over the past decade. These tokens are generally issued by independent ‘miners’ (or nodes). The innovative nature of this technology lies in the mechanisms through which the process to verify transactions is conducted by unknown, independent third parties without relying on a central manager. Blockchain is a type of distributed ledger where each transaction is verified using encryption keys and digital wallets; the numbers of the transactions are recorded on a new electronic distributed ledger, which is then connected through a chain (using hash functions) to previous, proven distributed ledgers using the proof-of- -work process. There are currently over 2,000 digital coins with features that vary substantially. Those tokens can be exchanged for some goods and services in many countries. Digital tokens are similar to cash since peer-to-peer transactions can be made instantaneously, 24 hours a day and 365 days a year (Table 1). All the transactions are anonymous but are technically traceable. A positive or negative interest rate can also be applied.

Many central banks and regulatory authorities do not regard these private digital tokens as ‘money’ because of their extreme price volatility. Consumers and investors are not well-protected since a regulatory framework is almost non-existent. As the technology evolves day by day, and various new digital tokens have been issued with diverse features, distributed ledger technology may conquer main technical and legal problems in the future, such as 51% attack and double-spending problems, scalability, substantial energy consumption, substantial volatility in values, vulnerability to cyber attacks, and potential anti-money laundering, and so on.

Four proposals on central bank digital currency

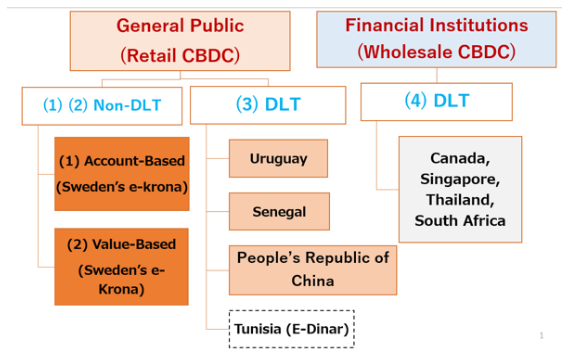

Some central banks have experimented with the application of digital tokens in their existing businesses by issuing their own digital tokens. These central bank digital currency proposals, together with the Swedish initiative to possibly issue bank accounts to the general public, can be classified into ‘retail CBDC’ and ‘wholesale CBDC’. The proposals can be further classified into CBDC not based on distributed ledger technology and CBDC based on distributed ledger technology. Figure 2 summarises all the CBDC proposals by classifying them into the following four types: (1) account-based retail CBDC without distributed ledger technology, (2) value-based retail CBDC without distributed ledger technology, (3) retail CBDC based on digital ledger technology, and (4) wholesale CBDC based on distributed ledger technology. All of these CBDCs are digital currencies.

Figure 2 Central bank digital currency proposals

Notes: DLT: distributed ledger technology; CBDC: central bank digital currency.

Source: Prepared by the author.

Proposals one and two: Central bank digital currency without distributed ledger technology

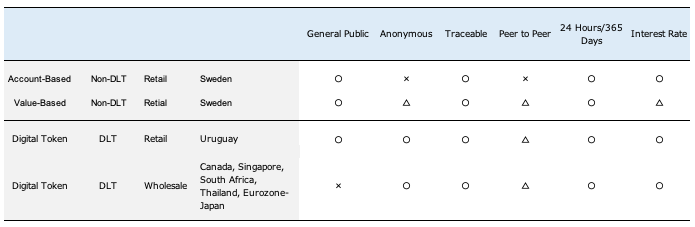

The Riksbank has been actively considering the first two proposals under the ‘e-krona’ project. The first, ‘account-based retail CBDC’ proposal is the issuance of a digital currency to the general public in the form of directly providing an account at Riksbank. The second, ‘value-based retail CBDC’ proposal is the issuance of a digital currency for which the prepaid value can be stored locally on a card or in a mobile phone application (digital wallets). All the transactions of both proposals are traceable since an underlying register enables the recording of all transactions and identification of the rightful owner of the digital e-krona (Table 2). Thus, transactions under the two proposals are non-anonymous because all transactions are identified. One exception of non-anonymity is the case of a prepaid e-krona card, on which e-krona are already stored and which can be used as cash and handed from one user to another. This is allowed as long as the payment amounts to less than €250 (to be lowered to €150 by 2020), as set by the EU. The Riksbank plans to experiment whether these proposals are, practically, implementable.

So far, most other central banks have not expressed an interest in these proposals. This is mainly because of concerns that commercial banks might suffer a loss in retail deposits from their accounts to those of a central bank, and would thus lose the sources of loan financing needed to extend credit to firms and individuals. This concern could be mitigated, however, if the central bank were to pay a lower interest rate to the general public than commercial banks do to their retail customers. Another concern is that bank runs may be exacerbated in the event of a banking crisis via a shift in deposits from commercial banks to the central bank, thereby deepening the crises. In addition, the amount of central bank notes in circulation has continued to rise in most countries, so there is no urgent reason for other central banks to examine these proposals at this stage.

As for monetary policy, it is technically possible for the Riksbank to impose a positive or negative interest rate under these proposals. From a legal standpoint, however, an interest rate can be only be applied to account-based e-krona and not to value-based e-krona, since the latter is regarded as ‘e-money’ and therefore should be a non-interest-bearing instrument according to the E-money Directive.

Table 2 Features of central bank digital currency proposals

Notes: DLT: distributed ledger technology; CBDC: central bank digital currency.

Source: Prepared by the author.

Proposal three: Retail central bank digital currency based on distributed ledger technology

Under the third proposal, CBDC has the features of anonymity, traceability, 24 hours a day and 365 days a year availability, and feasibility of an interest rate application (Table 2). The proposal is relatively popular among emerging economies, mainly because of a desire to take the lead in the rapidly emerging fintech industry, to promote financial inclusion by accelerating the shift to a cashless society, and to reduce cash printing and handling costs. Some countries – including Ecuador, Israel, Uruguay, Lithuania, the Marshall Islands, Tunisia, China, and Venezuela – have examined and/or conducted related experiments (Shirai 2019).

In sharp contrast to emerging economies, central banks in advanced economies are not enthusiastic about this proposal (Cœuré 2018). This reflects the fact that existing retail payments and settlements systems have become more efficient and faster and are available 24 hours a day and 365 days a year in some economies, so there is no strong case for promoting the proposal. Second, the use of cash is not yet declining. Third, almost all citizens are banked, so financial inclusion is not an urgent issue that needs to be tackled by a central bank. Fourth, many central banks do not wish to create competition between central bank money and private sector money and thus impose hardships on the existing banking system or amplify the resultant financial stability risk. Finally, central banks in advanced economies are generally more cautious than those in emerging economies because they fear harming their reputation should an initiative prove unsuccessful. Limited public interest and support for the proposal is another factor discouraging these central banks from actively considering the proposal.

Proposal four: Wholesale central bank digital currency based on distributed ledger technology

This proposal is the most popular among central banks because of the potential to make existing wholesale financial systems faster, less expensive, and safer. The Bank for International Settlements also shares the view that wholesale CBDC could potentially benefit the payments and settlements system. Since 2016, experiments have been conducted or examined by the central banks of countries including Canada, Singapore, Japan, Brazil, South Africa, and Thailand, as well as the euro area. The main purpose of these experiments was to promote the central bank’s understanding of the distributed ledger technology systems and their applicability in the existing wholesale financial markets, such as real-time gross settlement systems, delivery versus payment systems, cross-border interbank payments, settlements systems, and so on.

Most of the central banks concluded that their experiments successfully transferred digital tokens on a distributed ledger in real time and in reasonable volumes. Nevertheless, they have not taken further steps towards implementation because the current technology is seen as not yet sufficiently advanced to cope with privacy protection issues. The central banks believe the process of verifying transactions could be faster and most cost-efficient if the verifier is centralised (either through a group of selected commercial banks or a central bank), but this approach would not necessarily be superior to the existing system. In addition, their current wholesale payments and settlements systems are already sufficiently efficient, so no strong gains can be expected from a CBDC initiative.

Conclusions

In addition to central bank money and existing private sector money, digital currencies such as Bitcoin have emerged as potential private sector money. While their use as alternative payment tools currently remains limited, growing attention is being paid to their emergence because the underlying technology could enable a decentralised verification of transactions while maintaining attractive features similar to cash. Some central banks have examined the potential application of distributed ledger technology and issuing their own digital coins under ‘central bank digital currency’ proposals. So far, however, no central banks have found strong advantages to issuing their own digital coins due to technical constraints. An isolated move is noticeable in the case of Riksbank, which has been considering the issuance of deposit accounts or prepaid payment tools to the general public in the face of declining use of cash.

{kind=link}