This is an interesting little quantification of how Brexit has made us poorer. The value of exports is lower now Brexit is happening that it would have been without. Seems a reasonable enough calculation and answer too. It would also, to those in the know, count as being a blindingly obvious answer. For there’s this thing called the J Curve. Imports and exports are relatively inelastic in the short term, more so in the longer. The volume doesn’t change that much in the short term, while it does in the long, with respect to changes in price. On the other hand the value of imports and exports is almost entirely elastic. Because we measure that in money and foreign exchange markets move pretty quickly.

The result of this is that when we measure exports then we have a lag between the value change and the volume change. Measured by value exports can fall with a falling currency value. But only in the short term. That price change to foreigners does at some point become the dominant influence and exports rise as a result of the currency sinking. Thus that J in the J Curve. And this is as this paper has found. In the short term the fall in sterling has made UK exports worth less in U$. But it didn’t happen long enough ago for us to see the increase in the volume of exports translating into a rise in the value of. And that’s all they’ve found.

Oh, the usual rule of thumb for the J Curve to work itself out? 18 to 24 months after the fall in the exchange rate….

This paper is correct, it’s just not surprising nor useful. From The Conversation:

Brexit has already hurt EU and non-EU exports by up to 13% – new research

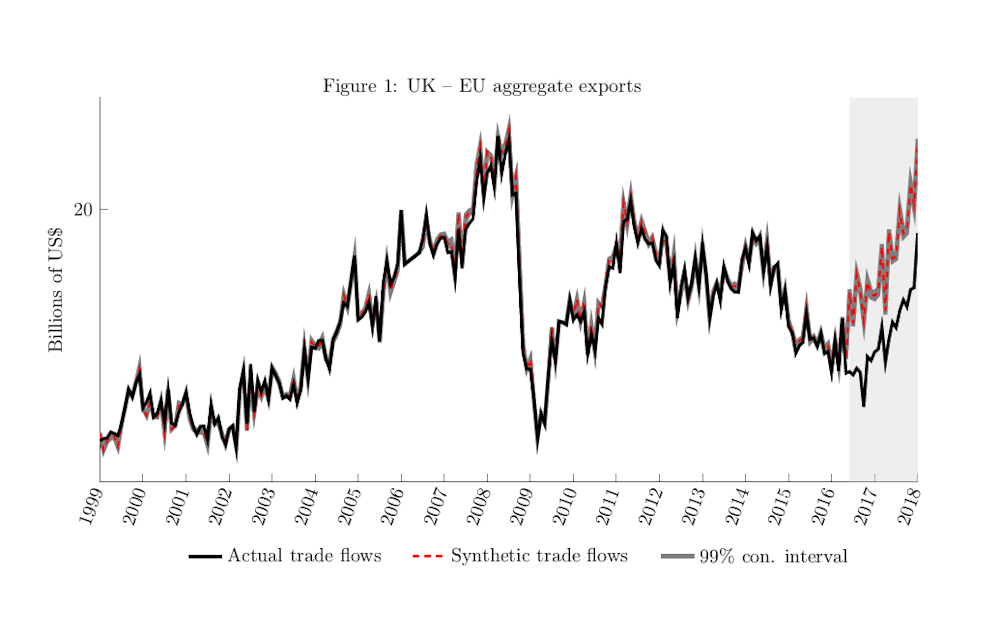

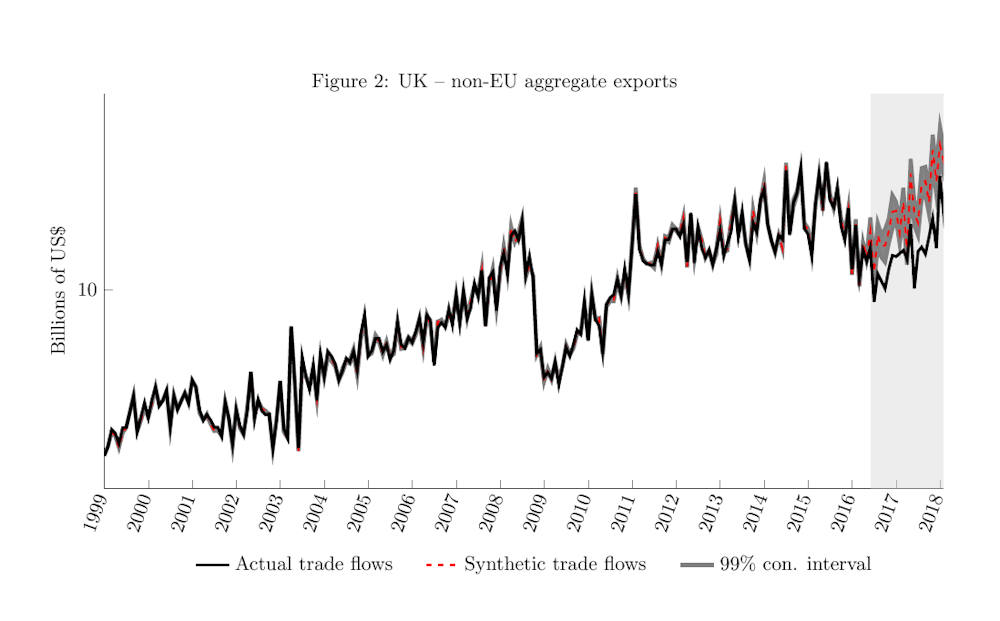

Over the past few months, we have been investigating how the vote of June 23 2016 has since affected the volumes and patterns of Britain’s trade with major trading partners inside and outside the European Union. By comparing trade flows with a model of what UK trade flows would have looked like had the UK voted to stay in the EU, we can clearly see that British exports to both EU and non-EU countries have taken a hit.

The very fact that Brexit hasn’t actually happened yet makes this question even more interesting to us as trade economists. No tariffs or trade barriers have been placed between the UK and EU, and yet companies are already aware that, depending upon the final deal, there may be substantial barriers within months. Several academic studies have emphasised that policy uncertainty is a major deterrent to trade, and the current Brexit negotiation period has been a good opportunity to test this.

It is a particularly good test because the Brexit vote came as such a shock: even on the day of the referendum, odds on Remain winning were about 9:2. A classic sign of surprise is the plunge of 10% to 15% in value of sterling against the dollar and euro within hours of the result.

In order to investigate the effects of the policy uncertainty and anticipation upon Britain’s exports and imports, we turned to the published monthly statistics for bilateral trade between the UK and 28 other countries (14 in the EU, 14 outside). These are currently available from 1999 to the first three months of 2018. We used these to predict what might have been expected to happen to the UK’s trade with each country in a counterfactual world where the Brexit vote had gone the other way.

A key assumption in our model is that the Brexit vote had a very strong shock upon trade flows involving the UK, but relatively little shock on flows which do not involve the UK. This allows us to compare how British trade levels have changed based on trade flows between other pairs of countries and, in doing so, we built a “synthetic doppelganger” for Britain’s trade in the months after the Brexit vote, using patterns of trade between other countries for unobservable shocks across countries such as changes in tastes and global business confidence. We also accounted for specific observable factors such as GDP and exchange rate changes.

Clear and consistent findings

We compared UK exports to and imports from each of the other 28 countries with a synthetic doppelganger. In all cases, the doppelganger and actual trade track each other closely up to the point of the referendum, after which there is a clear divergence.

For both UK exports to the EU and those to non-EU countries, we found a clear and consistent story: from the moment of the vote, British exports fall strongly behind the projected growth had there been no Brexit vote.

In both cases, the divergence is of a similar order of magnitude (8-13% before taking account of lagged exchange rate effects, or 13-16% without doing so). Interestingly, this is similar to the fall in sterling that followed the Brexit vote. This suggests that, through the fall in the pound, the UK started pricing its exports much more cheaply (in terms of dollars), but found few extra buyers, other than those we would have already expected, so the volume of exports moved in line with trade between our neighbours, but they were worth less due to the fall in sterling.

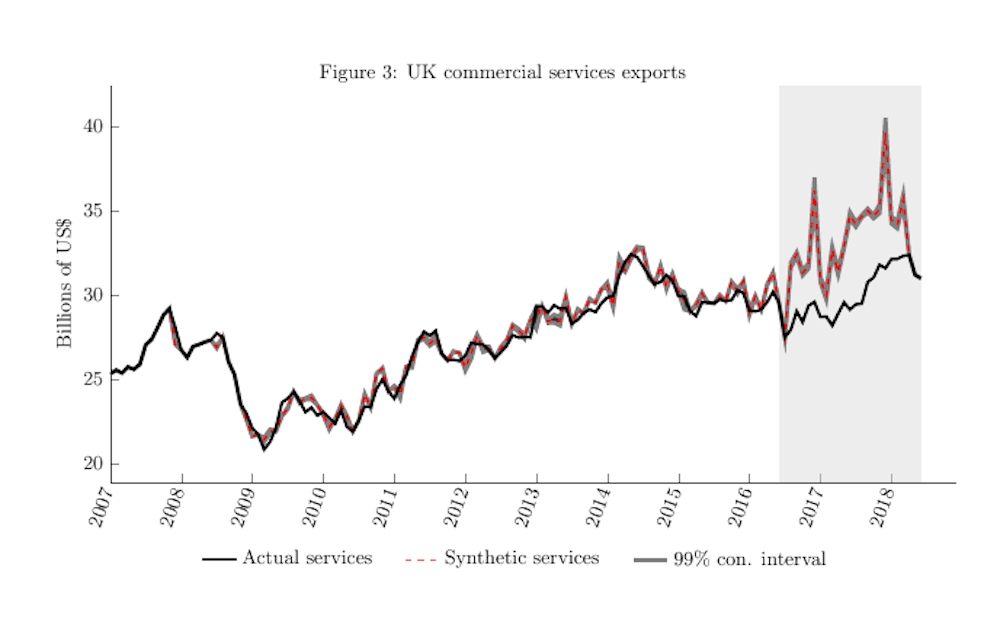

We also found commercial services exports – things like travel and tourism, transportation services, education, and banking, which are priced in US dollars – also stagnated for 18 months after the Brexit vote. This is at a time when world demand was growing.

In interpreting these poor export results, it is worth noting that there have been many reports of high export figures. But it’s important to recognise that these export numbers are measured in pound sterling and do not take into account the weakness of Britain’s currency. While there’s the appearance of a rise in exports, this is in large part due to the growth there’s been in global markets over the last couple of years.

Further, we argue that, since a significant amount of Britain’s exports are used to buy imports, what really matters is the value in terms of the currencies of our trading partners. If British exports sold can buy fewer imports, that translates to falling living standards at home, as imported goods rise faster in price than wages. Hence, Britain has lost a significant share in global markets (in terms of value) due to the uncertainties around Brexit, and is already poorer as a result.

{kind=link}

1. This paper had its conclusions before its evidence, I betcha.

2. It’s not about the money.

Mustapha Douch? Are we sure this isn’t an early Halloween prank?

The paper says that the $ value of exports has fallen in line with fall in the £:$ exchange rate because of Brexit which hasn’t happened yet.