Some number of thousands of initial coin offerings have now taken place. Many are duds, some are producing useful services off the back of the capital raising. And of the future? Maybe it’s all just too new to know but one good guess is they’re just part of the hype, the bubble, and that the market will fail as and when Bitcoin itself does:

Initial coin offerings: Fundamentally different but highly correlated

Antonio Fatás, Beatrice Weder di Mauro 26 March 2019

We should not expect a high correlation between ICO tokens and the price of Bitcoin or Ethereum given that they have very different business cases. This column demonstrates that this was indeed the case during 2007, but the moment the Bitcoin/Ethereum bubble burst, the correlation with ICOs increased and it remained high even when prices had stabilised. This may have been because the ICO market is still in its infancy and needs to mature, or it may indicate that ICOs were just one of the children of the hype and are likely to share the fate of major cryptocurrencies.

While the Bitcoin hype came under pressure in 2018 as its price collapsed, activity in initial coin offerings (ICOs) still remained significant. Over 1,000 new coins or tokens were created through ICOs in 2018, raising over US$21 billion.1 The two largest ICOs (pre-sale) – Telegram and EOS – raised $1.7 billion and $4.2 billion, respectively, and the next largest also raised over $500 million. Investors, aspiring entrepreneurs, and also policymakers and regulators have been paying increasing attention to this new market. What are the characteristics of ICOs? What are the benefits and risks? Do ICOs represent a new model of funding or is their fate linked to the world of cryptocurrencies?

ICOs as innovative funding models

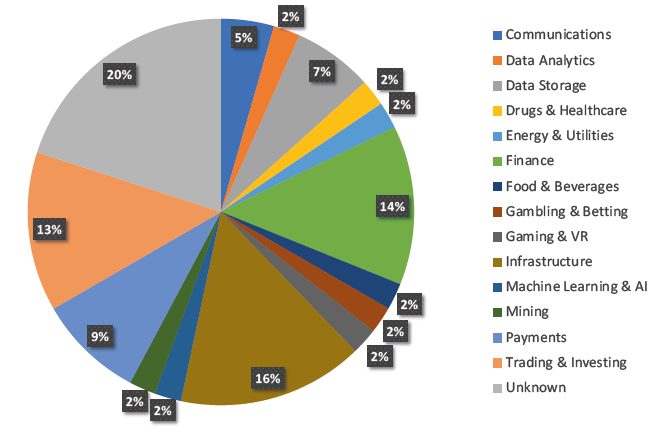

While ICOs typically rely on a similar technology to that used in cryptocurrencies (i.e. blockchain), their purpose is much wider than just facilitating payments. ICOs can be seen as a new funding model for new ventures. ICOs differ from traditional forms of funding because the founders often do not retain control of the platform after its launch, an attractive feature for those who like the idea of decentralised power. While many ICOs are in the IT space, there have also been many cases in other industries, ranging from health care, energy, and finance to infrastructure (see Figure 1).

Figure 1 Share of each sector in the 50 largest ICOs

Source: Author’s calculations based on list of largest ICOs at https://www.coinist.io/monthly-ico/

ICOs involve two types of tokens: security tokens and utility tokens. Security tokens offer participation in governance and future earnings, and are thus more akin to equity. Regulators have increasingly taken the view that the issuance of such tokens should be subject to the same regulations as securities, implying high regulatory costs.

To avoid potential regulation, most recent ICOs have involved utility tokens, where no ownership or dividends are granted to token holders. Utility tokens instead promise their holders access to the venture’s future services. This model works because most of the projects relate to building a platform around a community of users trading certain services (for example, Filecoin is a platform to exchange decentralised electronic storage services). As a result, the ICO not only raises the funding for the project but also puts into motion the launch of the network of future users.

The ICO funding model, like peer-to-peer lending, promises to reduce intermediation costs. But ICOs are more closely related to crowdfunding platforms, as the investment is linked to the use of the company’s product in a way that helps companies and markets better gauge the potential demand for the service, and it also creates a degree of customer commitment (Howell et al. 2018). The novelty of ICOs is that they promise ‘exclusive’ access to a service that is restricted to holders of a new token. For users of the platforms, tokens are the only way to purchase the service. And because demand is uncertain and possibly increases as the venture becomes successful, holders of tokens are often promised returns through increases in the value of the token.

Why is a new currency or token needed? Many ICO projects are related to platforms with strong network effects. Having investors committing to also being customers can create the necessary critical mass to make a project successful (Li and Mann 2018). This is what we observe empirically, with many ICOs are willing to underprice tokens in the initial phases in the hope of creating the necessary liquidity and critical mass (Momtaz 2018).

The limitations and risks of ICOs

While there are potential benefits to ICOs, there are also costs. The creation of separate tokens for services resembles a world in which products and services are priced in their own currency and transactions take place through barter, the equivalent to a modern “Stone Age world of the Flintstones” (Roubini 2018). This scenario runs contrary to the economic intuition that strong network effects of money of a single unit of account (i.e. one currency) always dominate a tokenised economy.

In addition, selling tokens to access future services and products requires a strong and verifiable commitment regarding the number of tokens or the price of the service (both of them related).2 The lack of a credible commitment technology could reduce the potential additional funding that the business might need and undermine the value of the ICO (Catalini and Gans 2018).

From the point of view of the investor, there can also be concerns about token values. Many early investors are betting on the popularity of the service associated with the token increasing so that the value of the token increases and delivers a return. But there can be a contradiction here – returns can only be realised when tokens are used, but tokens are only bought by investors speculating on a return.

The final potential risk is that ICOs do not have any inherent economic advantage, but are attractive simply because they offer a way of avoiding the regulatory costs related to securities laws and investor protection. In the worst-case scenario, they allow fraudulent projects to lure in small-time investors. The large number of ICOs that have failed provide support to these concerns.

The performance of ICOs as a funding vehicle

Because of the novelty of ICOs it is difficult to establish at this stage whether the potential benefits outweigh the risks and costs. Howell et al. (2018) provide evidence that successful ICOs have characteristics that are similar to successful projects that raise funds using alternative methods, reporting that “liquidity and trading volume are higher when issuers offer voluntary disclosure, credibly commit to the project, and signal quality”. On the other hand, Fisch (2018), using a similar methodology, finds mixed results.

Given the strong connection between ICOs and the world of cryptocurrencies, one of the fears has been that investors have bought ICO tokens because they were seen as a quick source of high returns. We now investigate whether ICO prices reflect this behaviour.

Our assumption is that there will be a positive correlation with returns on other cryptocurrencies because ICOs tend to rely on a similar infrastructure (many ICOs rely on Ethereum, for example). At the same time, the correlation cannot be too high given that the business model of Bitcoin or Ethereum, as alternative payment systems or token platforms, is quite different from the business models of most ICOs. As we have shown before, we find ICOs in a variety of sectors.

We study this correlation empirically by collecting data on the pricing of the largest 50 ICOs and test whether the behaviour of ICO returns are correlated to the returns of Bitcoin and Ethereum. If ICOs are truly pricing their unique business models, we would expect their returns to be idiosyncratic with low correlations. If, on the other hand, they are simply seen as an investment vehicle to generate excess returns based on a ‘cryptocurrency bubble’, we would expect them to be highly correlated to prices of the major cryptocurrencies.3

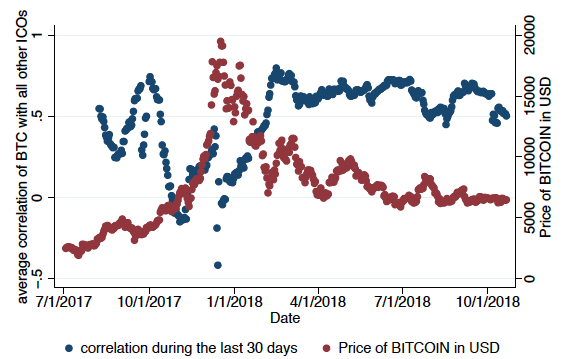

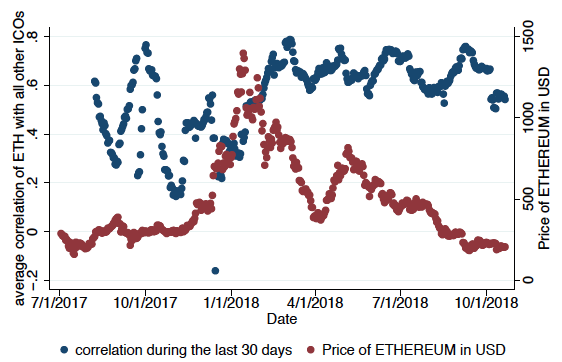

We calculate the daily correlation between the daily return of the top 50 ICOSs with the return of Bitcoin and Ethereum using a 30-day rolling window.4 The results are shown in Figures 2 and 3, where we plot the evolution of the price of the two cryptocurrencies in the same charts to understand whether the correlation has changed over time as the sentiment towards these currencies has changed.

Figure 2 Correlation of daily ICO returns with Bitcoin returns

Figure 3 Correlation of daily ICO returns with Ethereum returns

Correlations remained positive but low while the cryptocurrency phenomenon was taking off and Bitcoin and Ethereum prices were increasing. However, once the price of the two cryptocurrencies starts falling, correlations increase and reach a very high level, signalling that daily news on the future of Bitcoin and Ethereum seems to be moving the price of all ICO tokens. It seems that as the ‘cryptocurrency bubble’ bursts, the price-discovery mechanism of ICOs collapses and all their prices just track the value of Bitcoin or Ethereum.

Conclusions

ICOs are seen as funding vehicles and have been used to finance thousands of ventures in many different industries. We should not expect a high correlation between tokens and the price of Bitcoin or Ethereum given that they have very different business cases. This seems to have been the case during 2017, but the moment the Bitcoin/Ethereum bubble burst, the correlation with ICOs increased and remained very high even when prices had stabilised.

There are two interpretations of this pattern. The benign one is that the ICO market is still in its infancy and will need to mature. When ICOs grow up, we might expect them to be seen as very distant relatives of Bitcoin or Ethereum and to be priced according to their own merit. The alternative is that ICOs were just one of the children of the hype and are likely to share the fate of major cryptocurrencies.

{kind=link}