That there might be an interesting use or two of the blockchain part of Bitcoin technology is true. The jury’s still out on it and the market will, in the fullness of time, tell us. But should central banks be getting in on the act? Issuing a digital currency of their own perhaps? Hmm, well, depends what you’re after really:

All-new Echo Dot (3rd Gen) – Smart speaker with Alexa – Charcoal Fabric

Central bank digital currencies and private banks

David Andolfatto 17 March 2019

The idea of a central bank digital currency has prompted a mixed reaction among economists. This column uses a simple theoretical framework to investigate the impact of such a currency on a monopolistic banking sector. There are two main results. First, the introduction of an interest-bearing digital currency increases financial inclusion, diminishing the demand for physical cash. Second, while an interest-bearing digital currency reduces monopoly profit, it need not disintermediate banks in any way. A central bank digital currency may, in fact, lead to an expansion of bank deposits if the resulting competition compels banks to raise their deposit rates.

The recent surge of interest in privately issued cryptocurrencies has led a number of economists to investigate the possibility of central bank versions of a digital currency (e.g. Bech and Garratt 2017, Engert and Fung 2017, Kahn et al. 2019). Some, like Bordo and Levin (2017), see a great deal of merit in the proposal. Others, like Cecchetti and Schoenholtz (2017), see less benign consequences. These authors express major worries over the potential repercussions of a central bank digital currency (CBDC) on bank funding, bank credit, and financial market stability – a concern also raised by Bank of England Deputy Governor Ben Broadbent (Broadbent 2016).

Unfortunately, there is not much in the way of evidence or even theory to help shape our views on the matter.1 In a recent paper (Andolfatto 2018b), I develop a simple theoretical framework to help organise our thinking on the question of how the introduction of a CBDC is likely to impact private banks with market power. Perhaps not surprisingly, I find that the effects are likely to depend on monetary policy and the regulatory landscape. Nevertheless, I think it is of some interest to identify exactly how and why this may be the case.

My framework of analysis combines a version of the Diamond (1965) overlapping-generations model of government debt with the Klein (1971) and Monti (1972) model of a monopoly bank. There are two types of individuals populating the economy, which I refer to as ‘workers’ and ‘investors’. Workers supply the labour that is needed to produce goods and services. Investors have the capacity to transform this labour into a capital good that yields a future return of goods and services. Essentially, investors need to borrow labour and workers want to save for the future. In an ideal world, investors and workers would form cooperatives, with labour and capital combined to produce output that is shared between them. But in my model people are non-cooperative and do not fully trust each other, so an exchange medium is necessary (Gale 1978). In particular, I assume that investor–worker credit arrangements are not practical – workers will only accept money on a quid pro quo basis for labour services rendered.

Money takes the form of interest-bearing bank deposit liabilities (digital currency) and zero-interest physical currency (cash).2 Digital currency can be issued by the private bank and the central bank. In either case, it is made redeemable on demand at par for cash. The private bank has a reserve account with the central bank. Monetary policy consists of setting a policy interest rate that, for simplicity, serves as both a lending and deposit rate for the private bank. That is, the private bank may earn interest on reserves if reserve balances are positive, or it may hold negative reserve balances and pay the policy rate on borrowed reserves. Non-bank individuals can hold deposits with the central bank that yield a different interest rate (the ‘CBDC rate’). I assume that non-bank deposits with the central bank cannot be negative. That is, only the private bank is permitted to extend credit to individuals.

Workers in my model differ in terms of their income and face a fixed cost of accessing the bank sector. Consequently, low-income workers in my model will choose to remain unbanked, and must be paid in cash. High-income workers choose to access the interest-bearing deposit accounts made available by the central and private bank. The share of workers choosing to access the bank sector is shown to be increasing in the deposit rate offered by banks. I assume that both central and private banks offer the same payment services so that depositors are indifferent as to where they hold their money. As a result, the private bank will be compelled to offer at least the CBDC rate on its deposits if it is to retain its depositor base.3

Let me now describe the nature of economic activity in my model. At the start of a period, investors need to borrow money to finance their payroll of workers who are employed in the construction of capital. Investors can only acquire funding from the private bank. As a first pass, I assume that investment projects are risk-free and that investors can be relied upon to repay their bank loans. The private bank creates money in the act of lending, crediting each investor’s bank account by the amount of the money loan. The model has the intuitively plausible property that the volume of bank lending and capital investment is decreasing in the lending rate. The private bank charges lenders the profit-maximising lending rate which, for the monopolist, trades off profit margin against loan volume. Having acquired a money loan, investors pay their banked workers by deposit transfer and pay their unbanked workers with cash. Workers save their money, which they use to purchase goods and services in the future. Investors use sales of their future output to repay their bank loans and to finance their own consumption.

The model’s main proposition asserts that, absent binding liquidity constraints, the private bank’s lending behaviour is unaffected by the CBDC (in particular, the CBDC interest rate). This result is a consequence of the fact that, for the Klein-Monti monopoly bank, the profit margin on loans is determined by the lending rate net of the central bank’s policy rate, which represents the opportunity cost of commercial lending.4 The absence of any binding regulatory constraint – such as a reserve or capital requirement, a liquidity-coverage ratio, or a restriction on the amount of reserves that can be borrowed – plays an important role in generating this result. But what this shows is that it is not the CBDC per se that can be expected to impact bank lending; rather, it is the way in which the regulatory framework may interact with the CBDC competition that potentially alters the monopoly bank’s lending practices. The regulatory framework can, of course, be changed to suit the needs of the public.

If the CBDC does not affect bank lending, then what does it affect? The model is very clear on this. As long as the CBDC interest rate is below a positive policy rate, the CBDC has the effect of compelling the monopoly bank to increase the deposit rate it offers its customers. The reason for this is because the profit margin on deposits is the difference between the policy rate (e.g. interest on reserves) and the deposit rate. As long as the policy rate is positive, the monopoly bank will always find it profitable to at least match the CBDC interest rate. So in reality, even if the take-up of the CBDC is small, its mere existence may be enough to encourage more attractive terms for depositors. In my model, a higher deposit rate has the effect of increasing financial inclusion – more workers are induced to substitute out of cash and into interest-bearing bank deposits, which leads to an increase in the banking sector’s depositor base. Not surprisingly, the CBDC also reduces bank monopoly profits.

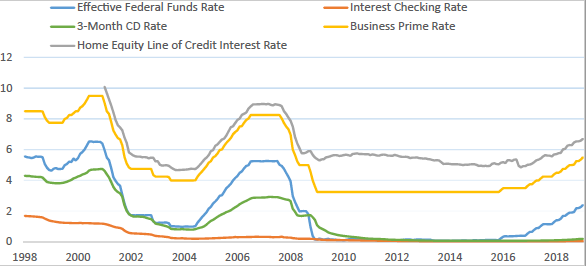

What of financial stability concerns? It is difficult to see how the introduction of one more risk-free, interest-bearing government security is likely to be destabilising. True, banks may witness deposit outflows, but they can choose to stem those outflows by offering depositors better terms. The capacity to do so seems evident, at least in the US, judging by the current spread between bank lending and deposit rates (see Figure 1). But even in the event of a large deposit outflow, an interest-targeting central bank should be willing to let banks borrow reserves. As with other considerations, the potential impact of a CBDC on banks and financial markets depends on the policies governments have in place (e.g. Grey forthcoming). It would be of some interest to check the sensitivity of my theoretical results by extending my model to incorporate factors that are missing but potentially important, such as bank and investment risk, moral hazard, regulatory considerations, and open economy considerations.

Figure 1 US interest rates, January 1998 to January 2019 (%)

Sources: RateWatch, Bloomberg and Federal Reserve Board.

Let me conclude with the following observation. In the US today, there exists an efficient, low-cost, real-time gross settlement payment system that transfers close to $3 trillion of funds per day across a set of fully insured digital accounts presently yielding 240 basis points in interest. Only depository institutions have access to this service (known as Fedwire) through the reserve accounts they hold with the US Federal Reserve. The rest of the US population must content itself with relatively slow payments, low deposit rates, high interchange fees, limited deposit insurance, or the inconvenience of cash. A significant number of Americans (over 8 million households) do not even have bank accounts. At the same time, the US Treasury permits all US persons to open online interest-bearing treasury accounts, called a TreasuryDirect account.5 Unfortunately, the existing infrastructure does not permit TreasuryDirect accounts to be used as a convenient payment instrument. However, this is clearly just a technical detail that could be modified with an appropriate change in public policy. Ricks et al. (2018) provide a strong case for why such a change is desirable.

{kind=link}