This is reposted from Medium where it seems to have died a death without any readers:

This isn’t a good start to trying to solve or rectify a problem

A useful guide to being able to solve a problem is to first understand what has caused it. We’ll not, for example, get far trying to treat the general paralysis of the insane with psychotherapy. Nor even psychiatry. A decent dose of penicillin some decades earlier is going to be a better solution to tertiary syphilis. Grasp what is causing the problem before we try to craft the solutions, that’s my motto.

Sadly, it seems not to be quite so well established in Kamala Harris’ policy team. For their plan to reduce the racial wealth gap is failing to understand why the gap exists in the first place. Thus the solutions proffered are unlikely to solve the problem.

They start with noting that there’s a significant difference in racial wealth — or median wealth when we slice and dice the population by race. This is true. It’s even something we’d like to do something about. But what we do does rather depend upon our grasping why this disparity exists. This, I maintain, is not what is being done.

Black and minority families were also disproportionately impacted by the subprime mortgage crisis and the subsequent Great Recession. Throughout the subprime market, Black borrowers were subjected to higher cost and higher risk loans than white borrowers, even when both had similar levels of creditworthiness. During the years of recovery, 2009–2011, the wealth gap between white households and households of color widened in part due to housing-market weakness.

Today, nearly three-quarters of white households (73%) are homeowners, while under half of Black households (45%) and Latinx households (47%) are homeowners. This percentage of Black homeowners has remained basically unchanged since 1968.

Now all of that’s true. And yet it’s not the whole and complete truth, something that will aid us in understanding the problem. For we have managed to substantially increase that black homeownership rate. As we can see from the very useful FRED database:

Well, how did we do that? In that orgy of the housing frenzy we progressively lowered deposit requirements, raised income multiples, so that people who previously couldn’t buy a house now could. And of course it all turned to shit. Because we ended up with large numbers of people who couldn’t really afford to buy a house buying a house.

No, this isn’t to make claims about how the Clinton Administration forced banks to lend to poor people in poor areas or anything, not to claim that the push against the old practices of redlining was excessive or anything. Those who want to make such claims are at liberty to do so, speech is free after all. Here we’re only noting that underwriting standards were relaxed and it didn’t work out well. As in fact the Harris campaign is complaining it didn’t in the first paragraph of that quote.

So, what is going to be our strategy this time around?

Our plan will create a 100-billion-dollar U.S. Housing and Urban Development (HUD)-administered grant to provide up to $25,000 in down payment assistance and closing costs. According to research from the Urban Institute, in early 2018, first-time homebuyers bought houses worth $245,320 with an average down payment of $22,561, and an interest rate of 4.43%.

This $100 billion investment will provide at least 4 million families/individuals living in federally-supported or renting housing in these historically red-lined communities with down payment and closing cost assistance.

We’re going to lower the deposit requirements again, are we? And our belief that it’ll work out well this time around is based upon what? Perhaps we should demand a little more justification for public policy than just hope.

That insistence upon redlining is interesting. Yes, we all do know of the historic practice. Yes it was appalling. And yet:

The grantee must have lived for at least the preceding 10 years in a historically red-lined community that remains low-to-moderate income.

Well, we know why this is here. Only the people who have lived in these historically disadvantaged areas will be aided to buy in them. The reason being that if outsiders could move in we might face that modern horror, gentrification. Personally I can’t see the problem with enough hipsters moving in to support a Whole Foods store. Would solve the food deserts problem rather nicely. I’m also aware that public opinion in general isn’t with me on this.

There is a basic problem with the idea though. Those low and moderate income areas. Those places that were redlined. They were the nice parts of town, were they? Places where housing gained substantial value?

To use the racially charged language of back then — the honky oppressors were restricting the coloreds to the good and desirable housing on the right side of the tracks, were they? Just the places where the would be upwardly mobile would like to be able to spend 30 years paying off a house loan? Or have we, by the construction of our program, decided that we’re only going to subsidise black people buying houses in the slums? Which almost sounds like the inverse of redlining coming back.

As you can tell I’m not enamoured of the solution here. But I think it’s worse than that, I don’t think they’ve understood the problem.

There is indeed a racial wealth gap. But to solve it we’ve got to know why it exists. Blaming Jim Crow might be satisfying, possibly even electorally useful, but it might not be the analysis we need to actually understand what is going on. Start from the fount of all knowledge concerning the wealth distribution, Saez and Zucman. Who point out that:

… Since the bottom half of the distribution always owns close to zero wealth on net,…

This is important. The bottom half of society isn’t really ever expected to have much wealth. Partly this is a lifetime cycle effect. We don’t expect students newly out of college — with their loans hanging around their necks — to have much wealth. While we’d rather hope that those on the cusp of retirement do have wealth both in housing equity and pensions funds. But it’s also not entirely a lifetime effect. We do still expect those with lower incomes to have very much less wealth than they do income as a share of the total. Savings and investment are, as we could put it, geared to income.

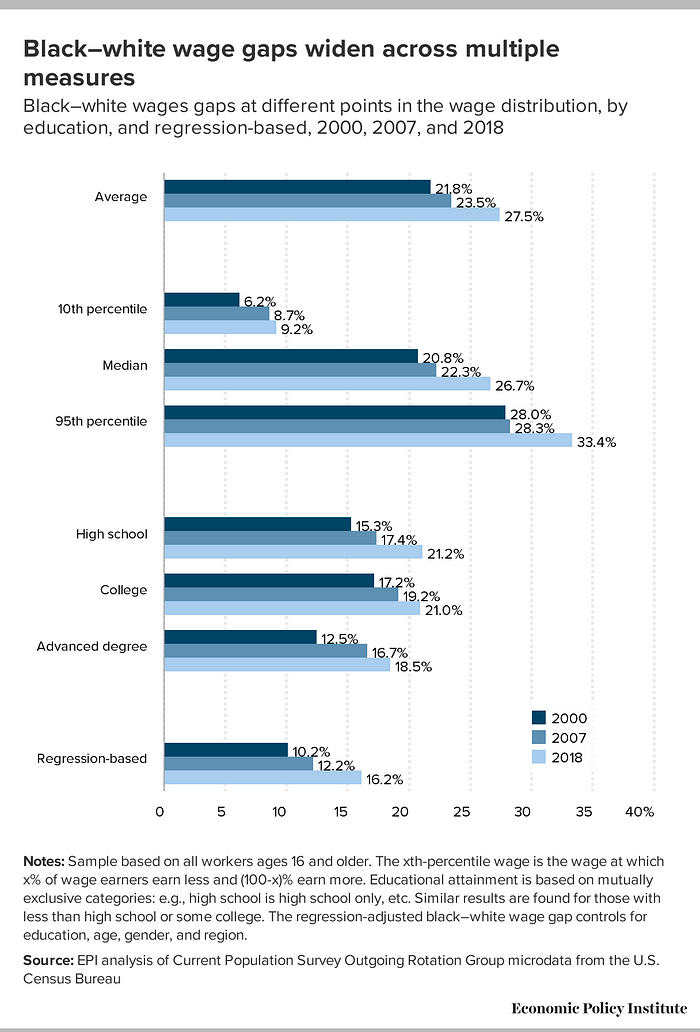

So some of our explanation is simply going to be that there is still a racial pay gap. Agreed, there shouldn’t be and yet there is. This is at least partly the cause of the wealth gap:

As to why this exists that’s more than I want to go into here. Although I’d strongly suspect that the appalling state of the inner city schooling systems has more than just a little bit to do with it. We should, for the purposes of the logic here, just see that it exists and take that as being read for the moment.

And yet there’s more to it than this. Because those wages there are as individuals. Yet our wealth figures are about households. These are not the same thing. So, what about income by household, to match our wealth measurements?

If we do agree that wealth is geared to income then we’ve found our reason why black wealth is significantly lower than white. Because incomes are such. And no, it’s only partly because black workers earn less than white. There’s obviously something different about the composition of black households too. The difference between black and white household income is very much larger — like twice the size — than the difference between black and white wages. Therefore there must be something different about black household composition.

Which there is:

Nope. No moral point being made there at all. As long as the conception is mutually agreed — or a happy accident at worst — I don’t care about the subsequent familial arrangements. Chacun a son gout as the enemy say. We must though recognise that we’ve a different familial structure here. So therefore such things as familial income are going to be different and we’ve already agreed that wealth is leveraged to income.

At least some part of the difference in black household wealth is because the black household is, on average, differently constructed to the white one. Again, there is no moral imputation here. It’s simply an observation, even if an important one. Because we’re never going to gain that desired economic equality unless we’re willing to decide upon equality of what? Equality of outcome given the same choices seems fair to me. A standard — look at the racial wage gap — which the US still doesn’t meet, I suspect significantly to do with the education system. But equality of wealth given different familial structures just isn’t going to happen, is it?

Which is what brings us back to what is wrong about Kamala Harris’ plan to beat the racial homeownership gap. It’s not based upon an understanding of why there’s the wealth gap in the first place. Therefore it would only be by some happy accident that it managed to address the underlying problem, not something that it does in fact manage.

Black and white households have different amounts of wealth — and part of that is homeownership, yes — because black and white people have, shamefully still, different incomes. Further the structures of black and white households are different. One, the incomes, is something we can and should do something about. The other? As a liberal I insist that people should indeed live their own lives their own way. Quite why we’d even want to change the familial structure of a culture within our society I’m not sure. But we’re going to have a wealth gap until we do.

{kind=link}

Would some sort of income-related mortgage relief work? So, not lowering the entry requirements, but the ongoing costs. MIRAS got me into home-ownership in 1992 along with a five-year starter discount rate and a 30-year term, and that was when interest rates were 15%!

“But to solve it we’ve got to know why it sexists.”

Dr Freud, Dr Freud to the white courtesy phone, please. Paging Dr Freud…

😉