It’s something between horrifying and delightful to see such a glorious missing of the point in this missive from Christine Lagarde concerning the gender diversity of the workforce. Horrifying that it has been missed, delightful to find that we’re ruled by those quite so blind – for it means that we can dismiss much else of what they say where we’re merely unsure if they’re wrong.

So, what she’s saying is that in many of the usual measures we can see that having a gender diverse workforce increases production for the same total labour input. This is because male and female workers are complements, not just substitutes.

Super, excellent, and can’t think of any reason why this won’t be true.

Which isn’t the point at all. Male and female labour are complements. There’s division and specialisation of labour in there. Not so much through innate skill as that biology has led to different average propensities. Hey, we’re mammals, viviparous, lactating, sexually dimorphic, all that. That evolution and history will have left us with different propensities is only an objectionable idea to the wilder believers in the Blank Slate in academia – where’s it’s an anathema.

Yes, obviously, note that this isn’t about individuals. We’re in that common realm where individual variation is greater than that of the averages between the two groups.

Note also that this is what Lagarde is already saying. There are these average differences between male and female labour.

OK. So why do we need to increase the female labour in the world of paid, market, labour? For we can all note that this complementarity, this division and specialisation, works in the fundamental human economic unit, the household. Again with the mammal, viviparous etc, combined with the unusually long childhood of our species.

Which is the point being missed. If male and female labour is different, as Lagarde insists, then why should all labour be forced into the market labour scene, instead of specialisation across market and household labour? As, actually, humans have historically done and still do. It, for example, being the entire and whole explanation of the gender pay gap, that men and women, on average, tend to change working habits differently in reaction to the arrival of children.

Another way of making the same point, if male and female labour is different then in what sector should each specialise?

The point isn’t even noted to be dismissed:

The macroeconomic benefits of gender diversity

Christine Lagarde, Jonathan D. Ostry 05 December 2018

The persistent gap between female and male labour force participation comes at a significant economic cost. This column argues that because women and men complement each other in the production process, the economic benefits from gender diversity are likely to be larger than suggested by previous studies. Gender complementarity also has important implications for the welfare costs from barriers to female labour force participation. The case for gender equity is even more compelling and pressing.

Although changes in cultural attitudes, childcare policies, and technologies have contributed to narrowing gender gaps over the past two decades, female labour force participation remains too low, with no advanced- or middle-income country having been able to reduce the gender gap below 7 percentage points. This continued uneven playing field between women and men comes at a significant economic cost.

Larger costs of barriers

Our analysis springs from the observation – supported by considerable microeconomic evidence – that women and men bring different skills and perspectives to the workplace, including different attitudes to risk and collaboration (Lagarde 2014). Women have been found to be more risk averse, reflecting greater fear of negative outcomes (Croson and Gneezy 2009), and to be more averse to competition (Harbaugh et al. 2002). Gender differences have also been linked to the nature of the job (Brussevich et al. 2018), to the stakes, and to time pressure. Hiring women can increase the productivity of women already employed in a firm, by reducing within-firm discrimination. In addition, studies have shown that the gender composition of a firm’s board affects its performance. Deszö and Ross (2012) find that for firms whose strategy is based on innovation, gender inclusiveness has positive effects on firm value, and Christiansen and others (2016) find that the effect of female representativeness in corporate boards is larger for firms in the services sector, high-tech manufacturing, and knowledge-intensive services. Gender diversity in boards of banking-supervision agencies has also been associated with greater financial stability (Sahay and Čihák 2018). Surprisingly, previous studies have not looked at the macroeconomic implications of this microeconomic evidence.

In the textbook neoclassical growth model, the labour force is the sum of the headcounts of male and female workers. Because replacing a man by a woman in this sum does not affect the labour force, there are no gains from gender diversity per se. Is this a reasonable assumption? This is an empirical question that needs testing.

Evidence on complementarity

The evidence – from macroeconomic, sectoral, and firm-level data – shows that women and men complement each other in the production process (Ostry et al. 2018). To gauge the extent of complementarity, we estimate the elasticity of substitution (ES) between women and men in the production function. The ES measures the change in a firm’s use of female labour (relative to the use of male labour) when the marginal productivity of female labour (relative to the marginal productivity of male labour) increases. When the ES is zero, it is impossible to substitute male labour for female labour because producing a good requires fixed proportions of each gender. When the ES approaches infinity, male and female labour are indistinguishable and there are no gains from gender diversity. Intermediate values of the ES imply that the labour of men and women complement each other to produce the final output.

We find that the estimates are clustered below 1 in the macro data, between 1 and 2 in the sectoral data, and between 2 and 3 in the firm-level data (Figure 1). The assumption that there are no complementarities between female and male workers is decisively rejected by the data. When female workers are initially in short supply relative to men, the effect of increasing female employment is larger than the effect of an equivalent increase in male workers as long as female productivity is not substantially lower than male productivity. Models that do not account for complementarity therefore underestimate the impact of gender diversity on growth, inappropriately attributing a part of growth to total factor productivity rather than to its real cause – past increases in female participation.

Figure 1 Range of estimates for the elasticity of substitution

Source: IMF staff estimates. See Ostry et al. (2018) for explanations.

Note: Midpoint is the baseline estimate. The box captures the range of estimates across models. Whiskers represent uncertainty related to the baseline estimate.

Men benefit from reducing barriers to female labour force participation

A key implication of our empirical analysis is that male wages are likely to rise as a result of narrowing gender participation gaps. There are two opposing effects from increasing female labour force participation (FLFP) on male wages. The first is the complementarity effect which increases productivity and thus male wages. The second is the capital-intensity effect which lowers wages as total labour supply increases. When the ES is below an estimated threshold of about 2.5 (as it is in our estimates), the first effect dominates and higher FLFP tends to boost men’s real wages. This is important because it should strengthen support for removing barriers that hold women back from productive participation in the labour force.

Bigger GDP gains

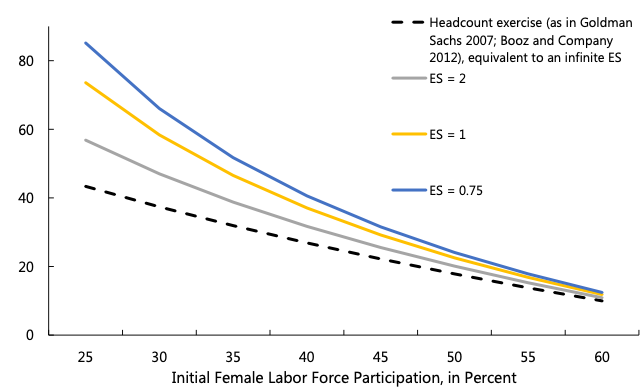

A second implication is that GDP gains from closing gender gaps are likely to be larger than we thought, based on models that do not account for gender complementarity. As shown in Figure 2, the range of estimates for the ES presented in Figure 1 imply that closing gender gaps in LFP could dramatically increase GDP, depending on the initial value of FLFP. Our calibration exercise suggests that, for the bottom half of the countries in our sample in terms of gender inequality, closing the gender gap could increase GDP by an average of 35%. Four fifths of these gains come from adding workers to the labour force, but fully one fifth of the gains is due to the gender diversity effect on productivity.

Figure 2 GDP gains from closing the gender gap in labour force participation

Source: IMF staff estimates.

Note: The calculations assume that there are constant returns to scale to labour, that male labour force participation is at 75 percent, and that women’s working hours are 17% lower than men’s. See Ostry et al. (2018) for explanations of the calculations.

Welfare considerations

The finding of gender complementarity – that gender diversity yields additional benefits – can also be incorporated into a model used to assess the welfare costs from different barriers to FLFP. The model disaggregates between the production of home goods and marketable goods to differentiate gains in GDP from gains in welfare. It also allows the number of women employed in different sectors to be driven by both the presence of barriers – capturing discrimination, cultural differences, social norms, and so on, which can affect either labour demand and/or supply – and the presence of potential differences in productivity across sectors. With services typically being a relatively more gender-equal sector, the model can be used to quantify the costs of barriers to FLFP when such barriers interfere with the process of structural transformation that is inherent in economic development.

The model, applied at the country level, suggests that only large barriers to FLFP can explain observed cross-country differences in FLFP. In particular, barriers are estimated to be equivalent to a 4 percent tax on female labour in the average country in Europe and Central Asia, but rising to the equivalent of a 53% tax rate on female labour in the average country in the Middle East and North Africa (MENA; see Figure 3). Significant gains in employment equality, income and welfare are therefore achievable by removing existing barriers. As an example, gains in welfare are likely to exceed 20% in the MENA and South Asia regions. Regional variation in welfare gains is explained by differences in the estimated barriers to FLFP and differences in initial income levels (welfare gains from increased production and consumption are larger in poorer countries).

Figure 3 Welfare and GDP gains from eliminating barriers to female labour force participation

{kind=link}

Hey, I’m doing my bit for gender equality by allowing people to refuse to employ me! Yay! Where do I get my medal?

So when female productivity equals male productivity ES is infinite. But the point where Madame Lagarde wants to increase female employment is when ES is 2.5. If that means the guy has to reduce the amount of overtime he works in order to do *some* housework because his wife has taken a part-time job it means either that he is far more efficient than she at housework or that she spends most of her time on other things.

Bah! What I should have said first of all is that increased female participation in the *reported* workforce increases *reported* GDP even if their is no real benefit. Using a nursery instead of swapping childcare with your neighbour alternate days increases reported GDP with, probably, a reduction in total welfare.

As soon as you see the word macroeconomic, you know it’s not worth reading any further.

Macroeconomics. Astrology meets alchemy.